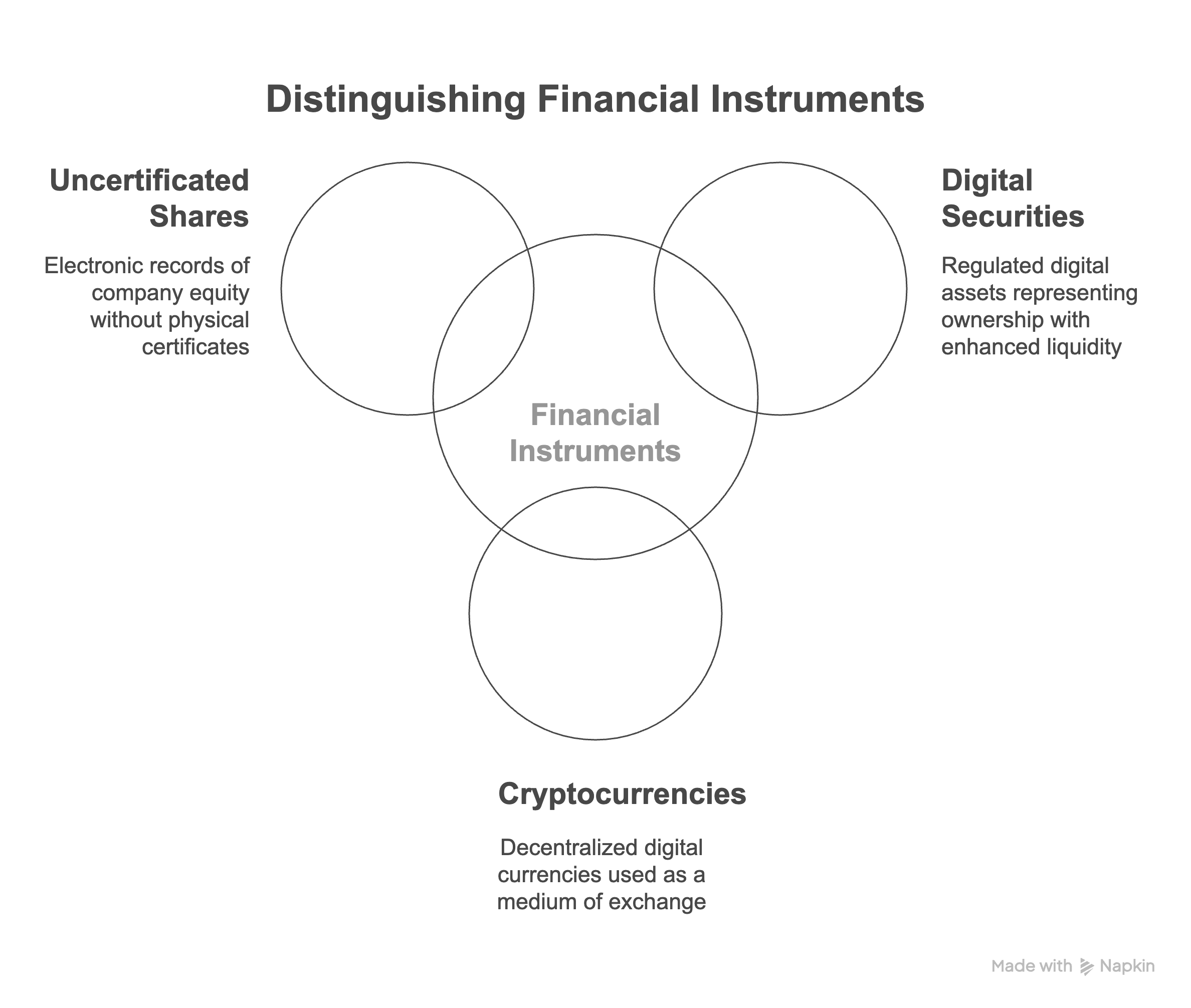

This article examines the key differences between digital securities, cryptocurrencies, and uncertificated shares - three distinct but often confused financial instruments in today's evolving financial landscape. Using the International Organization of Securities Commissions (IOSCO) Final Report "Policy Recommendations for Crypto and Digital Asset Markets" (November 2023) as the primary reference, this article clarifies their legal characteristics, regulatory treatments, and functional differences.

Digital Assets Securities Crypto and Shares Explained

0:00

/872.84

0:00

/0:25

1. Legal Foundations and Definitions

Digital Securities

Digital securities (sometimes called security tokens) are regulated financial instruments that represent ownership in an asset or company using blockchain or distributed ledger technology. They maintain the same legal status as traditional securities but exist in a digital form, providing benefits such as increased liquidity, fractional ownership, and streamlined transfer processes.

Cryptocurrencies

According to IOSCO's definitions, a "crypto-asset" is "an asset that is issued and/or transferred using distributed ledger or blockchain technology." Cryptocurrencies are a subset of crypto-assets primarily designed as a medium of exchange or store of value without representing ownership in another asset or company. Unlike digital securities, many cryptocurrencies are not primarily designed to function as regulated financial instruments.

Uncertificated Shares

Uncertificated shares are company equity that exists without physical certificates, represented instead by electronic records in a company's registry or through a central securities depository. They predate blockchain technology and are a legal evolution from paper share certificates to electronic record-keeping, generally still using traditional financial infrastructure.

2. Regulatory Framework Differences

Digital Securities

Digital securities fall clearly within existing securities regulation frameworks. They are subject to:

Full securities laws and regulations

Disclosure requirements

Registration requirements

Investor protection provisions

Secondary market trading rules

The IOSCO report emphasizes that digital securities should be regulated in a manner "consistent with IOSCO Objectives and Principles for Securities Regulation" regardless of their technological form.

Cryptocurrencies

The regulatory status of cryptocurrencies varies significantly by jurisdiction and is still evolving. The IOSCO report notes that many crypto-assets operate "in non-compliance with applicable regulatory frameworks or are unregulated." Cryptocurrencies may be subject to:

Varied treatment across jurisdictions (securities, commodities, payment instruments, or unique asset classes)

Emerging crypto-specific regulations

Anti-money laundering and counter-terrorist financing requirements

Less stringent disclosure obligations than securities

Regulatory gaps in investor protection

IOSCO emphasizes applying a principle of "same activities, same risks, same regulatory outcomes" to cryptocurrencies that function as economic substitutes for traditional financial instruments.

Uncertificated Shares

Uncertificated shares are firmly regulated under established securities laws and corporate governance frameworks. They are:

Subject to well-defined corporate and securities laws

Handled through regulated central securities depositories

Recorded in official shareholder registries

Protected by established investor protection mechanisms

Governed by existing company law provisions

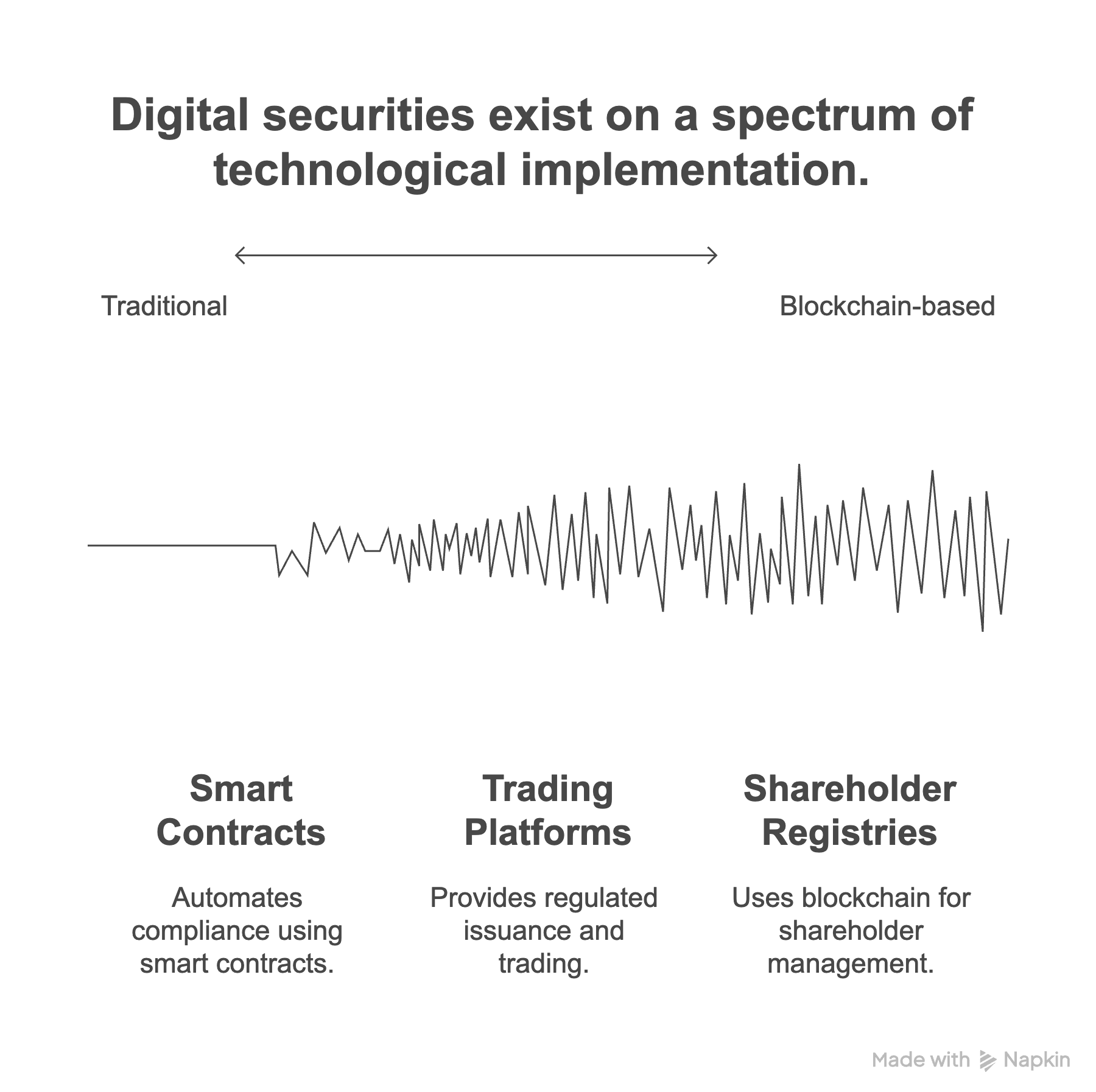

3. Technological Implementation

Digital Securities

Digital securities leverage blockchain technology to represent traditional securities, with:

Programmable compliance features ("smart contracts")

Regulated issuance and trading platforms

Integrated transfer restrictions and investor verification

Blockchain-based shareholder registries

Security features from both traditional finance and blockchain systems

Native tokens created within their blockchain environment

Often decentralized governance and development

Various consensus mechanisms (Proof of Work, Proof of Stake, etc.)

Limited or no intrinsic connection to external assets or companies

Focus on network security and integrity rather than securities compliance

Uncertificated Shares

Uncertificated shares typically use traditional database systems:

Centralized record-keeping through trusted intermediaries

Book-entry systems maintained by central securities depositories

Traditional authentication and security measures

No blockchain or distributed ledger technology required

Reliance on trusted third parties for verification and transfer

4. Asset Representation and Rights

Digital Securities

Digital securities represent:

Legal ownership in a company, asset, or financial instrument

Defined shareholder or creditor rights

Entitlement to dividends, voting rights, or interest payments

Claims on underlying assets or company value

Rights protected under securities laws

Cryptocurrencies

Cryptocurrencies typically:

Do not represent ownership in an external asset or company

Provide limited or no legal rights against any issuer

Derive value primarily from market demand and utility

Confer network participation rights rather than corporate rights

Often lack traditional legal remedies for holders

The IOSCO report notes that "information asymmetries and the lack of client disclosures" are significant concerns in cryptocurrency markets, contrasting with the structured rights in securities.

Uncertificated Shares

Uncertificated shares provide:

Full corporate ownership rights identical to certificated shares

Standard shareholder protections under company law

Traditional corporate governance participation

Claims on company assets and profits

Legal protections equivalent to paper certificates

5. Custody and Asset Protection

Digital Securities

Digital securities custody combines elements of both traditional securities and blockchain systems:

Regulated custodians with fiduciary responsibilities

Digital wallets with institutional-grade security

Private key management by regulated entities

Segregation of client assets from proprietary assets

Regulatory oversight of custody practices

Cryptocurrencies

Cryptocurrency custody generally involves:

Storage of private keys rather than securities

Various wallet solutions (hot, cold, and warm storage)

Self-custody options without intermediaries

Custody solutions with varying regulatory oversight

Heightened technological risks (key loss, theft)

IOSCO emphasizes that "proper custody of Client Assets is reliant on the strength of a service provider's systems, policies and procedures as well as the legal arrangements governing the custody relationship" - a particular challenge in cryptocurrency markets.

Uncertificated Shares

Uncertificated shares custody follows traditional securities practices:

Established custody through regulated financial institutions

Central securities depositories as ultimate record-keepers

Clear legal framework for ownership and transfer

Standardized reconciliation processes

Well-defined client asset protection rules

6. Market Infrastructure and Trading

Digital Securities

Digital securities trade on:

Regulated security token exchanges

Alternative trading systems for digital assets

Platforms with mandatory know-your-customer processes

Markets with pre-trade and post-trade transparency requirements

Systems with integrated compliance mechanisms

Cryptocurrencies

Cryptocurrencies trade on:

Crypto exchanges with varying degrees of regulation

Decentralized exchanges without central operators

Peer-to-peer trading platforms

Markets with limited transparency requirements

Systems primarily focused on transaction execution rather than compliance

IOSCO notes that, unlike regulated exchanges, many crypto trading platforms "combine multiple functions, including exchange services, brokerage, market-making and other proprietary trading, custody, clearing, settlement, and services relating to lending and/or staking" - creating significant conflicts of interest not permitted in traditional securities markets.

Uncertificated Shares

Uncertificated shares trade on:

Traditional stock exchanges and regulated markets

Alternative trading systems for securities

Broker-dealer networks with established regulations

Markets with standardized clearing and settlement

Systems with robust investor protection mechanisms

Conclusion

Digital securities, cryptocurrencies, and uncertificated shares represent three distinct financial instruments with significant differences in their legal status, regulatory treatment, technological implementation, and market infrastructure.

Digital securities combine elements of traditional securities regulation with blockchain technology, maintaining the legal protections of securities while leveraging technological innovations. Cryptocurrencies operate in a more evolving regulatory landscape, often with less investor protection and greater technological focus. Uncertificated shares represent the dematerialization of traditional securities without the distributed ledger component, maintaining all traditional securities protections.

As IOSCO's recommendations suggest, regulatory approaches should focus on the economic substance and function of these instruments rather than their technological form, ensuring appropriate investor protection regardless of the technological medium. Understanding these distinctions is crucial for investors, regulators, and market participants navigating this evolving landscape

Detailed Timeline

Prior to 2025 (Ongoing Development): Various jurisdictions begin exploring and developing regulatory frameworks for digital securities, applying existing securities laws like the Howey Test (US), MiFID II (EU), and existing regulations in the UK, Hong Kong, Singapore, Japan, Australia, Dubai, and Switzerland. Regulatory bodies such as the US Securities and Exchange Commission (SEC), UK Financial Conduct Authority (FCA), Hong Kong Securities and Futures Commission (SFC), and Monetary Authority of Singapore (MAS) issue guidance and frameworks.

Ongoing Development (Specific to UK): The UK Financial Conduct Authority (FCA) establishes a Digital Securities Sandbox to allow for controlled testing of digital securities innovations under regulatory oversight.

January 2025: The European Union's Markets in Crypto-Assets Regulation (MiCA) comes into full force. While primarily regulating non-security crypto assets, MiCA explicitly clarifies that crypto assets qualifying as financial instruments (digital securities) are governed by existing securities regulations, particularly MiFID II.

Cast of Characters

Here are the principal people and regulatory bodies mentioned in the sources:

Securities and Exchange Commission (SEC) (United States): A US regulatory body responsible for protecting investors, maintaining fair and orderly markets, and facilitating capital formation. The SEC applies the Howey Test to determine if a digital asset is a security and is a key entity in regulating digital securities in the US.

Financial Conduct Authority (FCA) (United Kingdom): The conduct regulator for financial services firms and financial markets in the UK. The FCA applies existing securities regulations to digital securities and has established a Digital Securities Sandbox.

Securities and Futures Commission (SFC) (Hong Kong): The statutory body responsible for regulating the securities and futures markets in Hong Kong. The SFC's approach to digital securities has evolved, recognising them as traditional securities with a "tokenisation wrapper".

Monetary Authority of Singapore (MAS) (Singapore): Singapore's central bank and financial regulatory authority. MAS regulates digital tokens that qualify as securities under existing laws and has published a "Guide to Digital Token Offerings".

International Organization of Securities Commissions (IOSCO): An international body that brings together the world's securities regulators and is recognised as the global standard setter for the securities sector. IOSCO is working towards international regulatory alignment and common standards for digital securities regulation.

Glossary of Key Terms

Digital Securities: Regulated financial instruments representing ownership in an underlying asset or company, issued, recorded, and transferred using blockchain or distributed ledger technology (DLT).

Security Tokens: Another term for digital securities, emphasizing their representation of security ownership on a digital ledger.

Tokenized Securities: Similar to digital securities, highlighting the process of converting rights or assets into digital tokens on a blockchain.

Blockchain Technology: A distributed, immutable ledger system that records transactions across many computers.

Distributed Ledger Technology (DLT): A broader term encompassing blockchain and other distributed database technologies used to record transactions.

Howey Test: A legal test used in the US to determine if a transaction qualifies as an "investment contract" and is therefore subject to securities regulation.

Substance-over-form: A regulatory principle that focuses on the economic reality and function of a transaction or asset rather than its specific technological form or label.

Markets in Crypto-Assets Regulation (MiCA): An EU regulation establishing a legal framework for crypto assets, excluding those that qualify as financial instruments.

Markets in Financial Instruments Directive (MiFID II): An EU directive regulating financial markets and instruments, including securities.

Financial Conduct Authority (FCA): The regulatory body for financial services firms and markets in the United Kingdom.

Digital Securities Sandbox: A regulatory initiative allowing firms to test new technological innovations in a controlled environment with regulatory oversight.

Securities and Futures Commission (SFC): The regulatory body overseeing the securities and futures markets in Hong Kong.

Tokenisation Wrapper: A term used by the Hong Kong SFC to describe the technological layer provided by blockchain that encapsulates traditional securities.

Monetary Authority of Singapore (MAS): Singapore's central bank and integrated financial regulator.

Equity Tokens: Digital securities representing ownership (shares) in a company.

Debt Tokens: Digital securities representing a loan or bond.

Asset-Backed Tokens: Digital securities representing ownership in physical or financial assets.

Fund Tokens: Digital securities representing shares in an investment fund.

Derivative Tokens: Digital securities representing rights and obligations related to underlying assets (e.g., options, futures).

Prospectus/Offering Memorandum: Disclosure documents providing material information about a security offering and the issuer.

Intermediaries: Entities that facilitate financial transactions, such as trading platforms, broker-dealers, and custodians.

Customer Due Diligence (CDD): Processes undertaken by financial institutions to verify the identity of their clients and assess potential risks.

Suitability Assessments: Processes to ensure that financial products or services are appropriate for an investor's circumstances and objectives.

Cybersecurity Protocols: Measures and procedures designed to protect computer systems, networks, and data from theft or damage.

Private Key Management: The secure handling and storage of cryptographic keys that control access to digital assets.

Smart Contract Auditing: The systematic review and analysis of smart contract code to identify vulnerabilities, errors, or inefficiencies.

Permissioned Networks: Blockchain networks where participation is restricted and requires pre-approval from network administrators.

Public Networks with Compliance Layers: Open blockchain networks enhanced with additional technological or legal mechanisms to enforce regulatory requirements.

Smart Contracts: Self-executing programs stored on a blockchain that automatically carry out the terms of an agreement.

Custody Infrastructure: Systems and services for securely storing and managing digital assets on behalf of others.

Institutional-Grade Wallets: Secure digital storage solutions designed for financial institutions with advanced security features.

Multi-Signature Authentication: A security measure requiring multiple private keys to authorise a transaction.

Cold Storage Solutions: Offline methods for storing cryptographic keys, typically considered the most secure.

Segregated Account Structures: Arrangements that keep client assets separate from the assets of the firm holding them.

Fractional Ownership: The ability to own a portion or fraction of a high-value asset.

T+1/T+2 Settlement: Traditional settlement cycles where a transaction is completed one or two business days after the trade date.

Disintermediation: The reduction or removal of intermediaries in a transaction or process.

Immutable Records: Data stored on a blockchain that is resistant to alteration or deletion.

Counterparty Risk: The risk that one party to a financial contract will not fulfil its obligations.

International Organization of Securities Commissions (IOSCO): An international body that brings together the world's securities regulators.

References

Primary Source

International Organization of Securities Commissions (IOSCO). (2023, November 16). Policy Recommendations for Crypto and Digital Asset Markets - Final Report. https://www.iosco.org/library/pubdocs/pdf/IOSCOPD747.pdf

Additional References

Securities and Exchange Commission (SEC). (2025, April 10). Offerings and Registrations of Securities in the Crypto Asset Markets. https://www.sec.gov/newsroom/speeches-statements/cf-crypto-securities-041025

MME Legal Tax Compliance. (2019, April 23). Shares in the Digital Age. Lexology. https://www.lexology.com/library/detail.aspx?g=459524c7-56ef-4555-9371-6295af2e9683

Corporate Direct, Inc. (2025, April 15). The Difference Between Certificated And Uncertificated Securities. https://corporatedirect.com/asset-protection/the-difference-between-certificated-and-uncertificated-securities/

Skadden, Arps, Slate, Meagher & Flom LLP. (2023, June). IOSCO Proposes Policy Recommendations for the Regulation of Crypto Markets. https://www.skadden.com/insights/publications/2023/06/iosco-proposes-policy-recommendations

WilmerHale. (2023, July 11). Digital Assets Consultation Offers First Step In Regulation. https://www.wilmerhale.com/en/insights/blogs/wilmerhale-w-i-r-e-uk/20230711-digital-assets-consultation-offers-first-step-in-regulation

Thompson Coburn LLP. (2025, January 30). Fast Developments in Treatment of Crypto Assets Under Federal Securities Laws: Has A New Day Dawned? https://www.thompsoncoburn.com/insights/fast-developments-in-treatment-of-crypto-assets-under-federal-securities-laws-has-a-new-day-dawned/

Comments